import numpy as np

from scipy import stats, linalg, optimize

import statsmodels.api as sm

import matplotlib.pyplot as plt

plt.style.use('assets/book.mplstyle')

rng = np.random.default_rng(42)Appendix A — Python Scientific Computing Reference

This appendix is a reference, not a tutorial. It gathers the computational tools assumed by the main chapters in one place, with runnable examples and pointers to where each tool is used. If you know Python but have not worked with NumPy, SciPy, or statsmodels before, read this appendix first — it provides the vocabulary the rest of the book speaks in.

NumPy Essentials

NumPy is the foundation everything else sits on. Every chapter in this book creates, reshapes, slices, and combines arrays. This section covers the patterns that recur most often.

A.0.1 Array creation

The most common constructors:

# Zeros, ones, and identity

print("zeros(3): ", np.zeros(3))

print("ones((2,3)): \n", np.ones((2, 3)))

print("eye(3): \n", np.eye(3))

# Sequences

print("arange(0, 1, 0.3):", np.arange(0, 1, 0.3))

print("linspace(0, 1, 5):", np.linspace(0, 1, 5))zeros(3): [0. 0. 0.]

ones((2,3)):

[[1. 1. 1.]

[1. 1. 1.]]

eye(3):

[[1. 0. 0.]

[0. 1. 0.]

[0. 0. 1.]]

arange(0, 1, 0.3): [0. 0.3 0.6 0.9]

linspace(0, 1, 5): [0. 0.25 0.5 0.75 1. ]arange uses a step size and may or may not include the endpoint (floating-point rounding decides). linspace uses a count and always includes both endpoints — prefer it for grids where exact endpoints matter.

# From existing data

a = np.array([1.0, 2.0, 3.0])

print("array: ", a, "dtype:", a.dtype)

# Diagonal matrix from a vector

print("diag([1,2,3]):\n", np.diag([1, 2, 3]))

# Repeat and tile

print("repeat: ", np.repeat([1, 2], 3))

print("tile: ", np.tile([1, 2], 3))array: [1. 2. 3.] dtype: float64

diag([1,2,3]):

[[1 0 0]

[0 2 0]

[0 0 3]]

repeat: [1 1 1 2 2 2]

tile: [1 2 1 2 1 2]A.0.2 Indexing and slicing

NumPy arrays support integer indexing, slicing, boolean indexing, and fancy (array) indexing. Slices return views — modifying the slice modifies the original. Fancy indexing returns copies.

X = np.arange(12).reshape(3, 4)

print("X:\n", X)

# Basic slicing (views)

print("Row 0: ", X[0])

print("Col 1: ", X[:, 1])

print("Submatrix:\n", X[:2, 1:3])

# Boolean indexing (copy)

mask = X > 5

print("X[X > 5]: ", X[mask])

# Fancy indexing (copy)

rows = np.array([0, 2])

print("Rows 0,2: \n", X[rows])X:

[[ 0 1 2 3]

[ 4 5 6 7]

[ 8 9 10 11]]

Row 0: [0 1 2 3]

Col 1: [1 5 9]

Submatrix:

[[1 2]

[5 6]]

X[X > 5]: [ 6 7 8 9 10 11]

Rows 0,2:

[[ 0 1 2 3]

[ 8 9 10 11]]A.0.3 Broadcasting

Broadcasting lets NumPy operate on arrays with different shapes without explicit loops or copies. The rule: dimensions are compared from the right; they are compatible if they are equal or one of them is 1. A missing dimension is treated as 1.

# Scalar broadcast

a = np.array([1, 2, 3])

print("a + 10:", a + 10)

# Column vector + row vector -> matrix

col = np.array([[1], [2], [3]]) # shape (3, 1)

row = np.array([10, 20, 30, 40]) # shape (4,)

print("col + row:\n", col + row) # shape (3, 4)

# Centering columns of a matrix (subtract column means)

X = rng.standard_normal((4, 3))

X_centered = X - X.mean(axis=0) # (4,3) - (3,) -> (4,3)

print("Column means after centering:",

X_centered.mean(axis=0).round(15))a + 10: [11 12 13]

col + row:

[[11 21 31 41]

[12 22 32 42]

[13 23 33 43]]

Column means after centering: [ 0. -0. 0.]Broadcasting is used throughout the book — centering data (Ch. 11), evaluating densities on grids (Ch. 7), and computing pairwise distances (Ch. 19) all rely on it.

A.0.4 Common pitfalls

Three NumPy traps catch even experienced users. Recognizing them early saves hours of silent-bug debugging.

1. Views vs copies. Basic slicing returns a view that shares memory with the original array. Modifying the slice modifies the original — sometimes intentionally, often not:

original = np.array([10, 20, 30, 40, 50])

view_slice = original[1:4] # basic slice -> view

view_slice[0] = 999

# The original is now corrupted:

print(f"original after view mutation: {original}")

# Safe pattern: call .copy() when you need independence

original = np.array([10, 20, 30, 40, 50])

safe_copy = original[1:4].copy()

safe_copy[0] = 999

print(f"original after copy mutation: {original}")original after view mutation: [ 10 999 30 40 50]

original after copy mutation: [10 20 30 40 50]Boolean and fancy indexing always return copies, so a[a > 0] = 0 modifies a in-place but b = a[a > 0] produces an independent array. See the expanded discussion later in this appendix.

2. Integer vs float arrays. NumPy infers dtype from the input. An array created from integers will silently truncate floats:

int_array = np.array([1, 2, 3]) # dtype: int64

int_array[0] = 1.9

# The 1.9 is truncated to 1, no warning:

print(f"int array after assigning 1.9: {int_array}")

print(f"dtype: {int_array.dtype}")

# Safe pattern: specify float dtype at creation

float_array = np.array([1, 2, 3], dtype=float)

float_array[0] = 1.9

print(f"float array: {float_array}")int array after assigning 1.9: [1 2 3]

dtype: int64

float array: [1.9 2. 3. ]This trap surfaces when building arrays from counts or indices and later assigning computed values. Always create numerical arrays with dtype=float when they will hold non-integer results.

3. Shape (n,) vs (n, 1). A 1-D array with shape (n,) is not a column vector. Matrix operations that expect a column vector — or code that relies on 2-D broadcasting rules — will silently produce wrong shapes:

v = np.array([1, 2, 3]) # shape (3,)

print(f"v.shape: {v.shape}")

print(f"v.T.shape: {v.T.shape}") # transpose is a no-op!

# Outer product attempt: v @ v.T gives a scalar, not a matrix

print(f"v @ v.T: {v @ v.T}") # dot product = 14

# Fix: reshape to (3,1) to get a true column vector

v_col = v.reshape(-1, 1) # shape (3, 1)

print(f"v_col @ v_col.T:\n{v_col @ v_col.T}") # 3x3 outer productv.shape: (3,)

v.T.shape: (3,)

v @ v.T: 14

v_col @ v_col.T:

[[1 2 3]

[2 4 6]

[3 6 9]]When statsmodels or scipy expects a 2-D array and receives a 1-D array, the result is often a confusing shape mismatch error. Use x.reshape(-1, 1) to promote a 1-D array to a column vector, or np.atleast_2d(x).T for the same effect.

A.0.5 Reshape, ravel, and transpose

a = np.arange(12)

print("reshape(3,4):\n", a.reshape(3, 4))

print("reshape(3,-1):\n", a.reshape(3, -1)) # infer columns

M = a.reshape(3, 4)

print("ravel:", M.ravel()) # back to 1-D (view)

print("M.T:\n", M.T) # transposereshape(3,4):

[[ 0 1 2 3]

[ 4 5 6 7]

[ 8 9 10 11]]

reshape(3,-1):

[[ 0 1 2 3]

[ 4 5 6 7]

[ 8 9 10 11]]

ravel: [ 0 1 2 3 4 5 6 7 8 9 10 11]

M.T:

[[ 0 4 8]

[ 1 5 9]

[ 2 6 10]

[ 3 7 11]]Use -1 in one dimension to let NumPy infer it. ravel() returns a view when possible; flatten() always returns a copy.

A.0.6 Stacking and splitting

Combining arrays is a constant need — assembling design matrices, collecting bootstrap samples, or building block-diagonal structures.

a = np.array([1, 2, 3])

b = np.array([4, 5, 6])

# Vertical and horizontal stacking

print("vstack:\n", np.vstack([a, b]))

print("hstack: ", np.hstack([a, b]))

# column_stack: treat 1-D arrays as columns

print("column_stack:\n", np.column_stack([a, b]))

# concatenate: general-purpose

M1 = np.ones((2, 3))

M2 = np.zeros((2, 3))

print("concatenate (axis=0):\n",

np.concatenate([M1, M2], axis=0))vstack:

[[1 2 3]

[4 5 6]]

hstack: [1 2 3 4 5 6]

column_stack:

[[1 4]

[2 5]

[3 6]]

concatenate (axis=0):

[[1. 1. 1.]

[1. 1. 1.]

[0. 0. 0.]

[0. 0. 0.]]np.column_stack is the most common pattern in this book — it builds the design matrix \(\mathbf{X}\) from individual predictor vectors. np.vstack appears when stacking observation batches.

A.0.7 Useful functions

Several NumPy functions appear often enough to warrant a brief catalog:

x = np.array([-2.5, 0.3, 1.7, 4.2, -0.1])

# where: element-wise conditional

print("where(x>0, x, 0):", np.where(x > 0, x, 0))

# clip: bound values

print("clip(-1, 2): ", np.clip(x, -1, 2))

# searchsorted: binary search on sorted array

sorted_a = np.array([1, 3, 5, 7, 9])

print("searchsorted(4): ", np.searchsorted(sorted_a, 4))

# cumsum and diff

print("cumsum: ", np.cumsum([1, 2, 3, 4]))

print("diff: ", np.diff([1, 4, 6, 10]))

# einsum: Einstein summation (trace example)

A = np.array([[1, 2], [3, 4]])

print("trace via einsum:", np.einsum('ii', A))

print("matmul via einsum:\n",

np.einsum('ij,jk->ik', A, A))where(x>0, x, 0): [0. 0.3 1.7 4.2 0. ]

clip(-1, 2): [-1. 0.3 1.7 2. -0.1]

searchsorted(4): 2

cumsum: [ 1 3 6 10]

diff: [3 2 4]

trace via einsum: 5

matmul via einsum:

[[ 7 10]

[15 22]]np.einsum is the Swiss army knife for tensor contractions. It appears in Ch. 19 for multivariate statistics and in Ch. 14 for mixed-effects computations where explicit loops over groups would be slow.

A.0.8 Views vs copies: a common trap

Understanding when NumPy returns a view (shared memory) vs a copy (independent memory) prevents subtle bugs:

a = np.arange(5)

b = a[1:4] # slice -> view

b[0] = 99

print(f"a after modifying slice: {a}")

# a is modified because b is a view

c = a[[1, 2, 3]] # fancy index -> copy

c[0] = -1

print(f"a after modifying fancy: {a}")

# a is NOT modified because c is a copya after modifying slice: [ 0 99 2 3 4]

a after modifying fancy: [ 0 99 2 3 4]Rule of thumb: basic slicing produces views; boolean and fancy indexing produce copies. When in doubt, call .copy() explicitly. This matters in Ch. 9 (bootstrap resampling) where accidentally modifying the original data through a view would corrupt results.

Matplotlib Essentials

Every figure in this book is produced with Matplotlib. The book’s style sheet (assets/book.mplstyle) sets publication-quality defaults — serif fonts, suppressed top/right spines, a colorblind-friendly cycle with alternating line styles, and 300 dpi output.

A.0.9 The Figure/Axes model

Matplotlib distinguishes between the figure (the canvas) and one or more axes (the individual plots). The explicit axes API gives full control:

fig, ax = plt.subplots()

x = np.linspace(0, 2 * np.pi, 200)

ax.plot(x, np.sin(x), label="sin")

ax.plot(x, np.cos(x), label="cos")

ax.set_xlabel("x")

ax.set_ylabel("f(x)")

ax.set_title("Sine and cosine")

ax.legend()

plt.show()

For multiple panels, use subplots with rows and columns:

fig, axes = plt.subplots(1, 3, figsize=(10, 3))

t = np.linspace(0, 4 * np.pi, 300)

for i, (func, name) in enumerate([

(np.sin, "sin"), (np.cos, "cos"),

(lambda x: np.sin(x) * np.exp(-x / 5), "damped sin"),

]):

axes[i].plot(t, func(t))

axes[i].set_title(name)

fig.tight_layout()

plt.show()

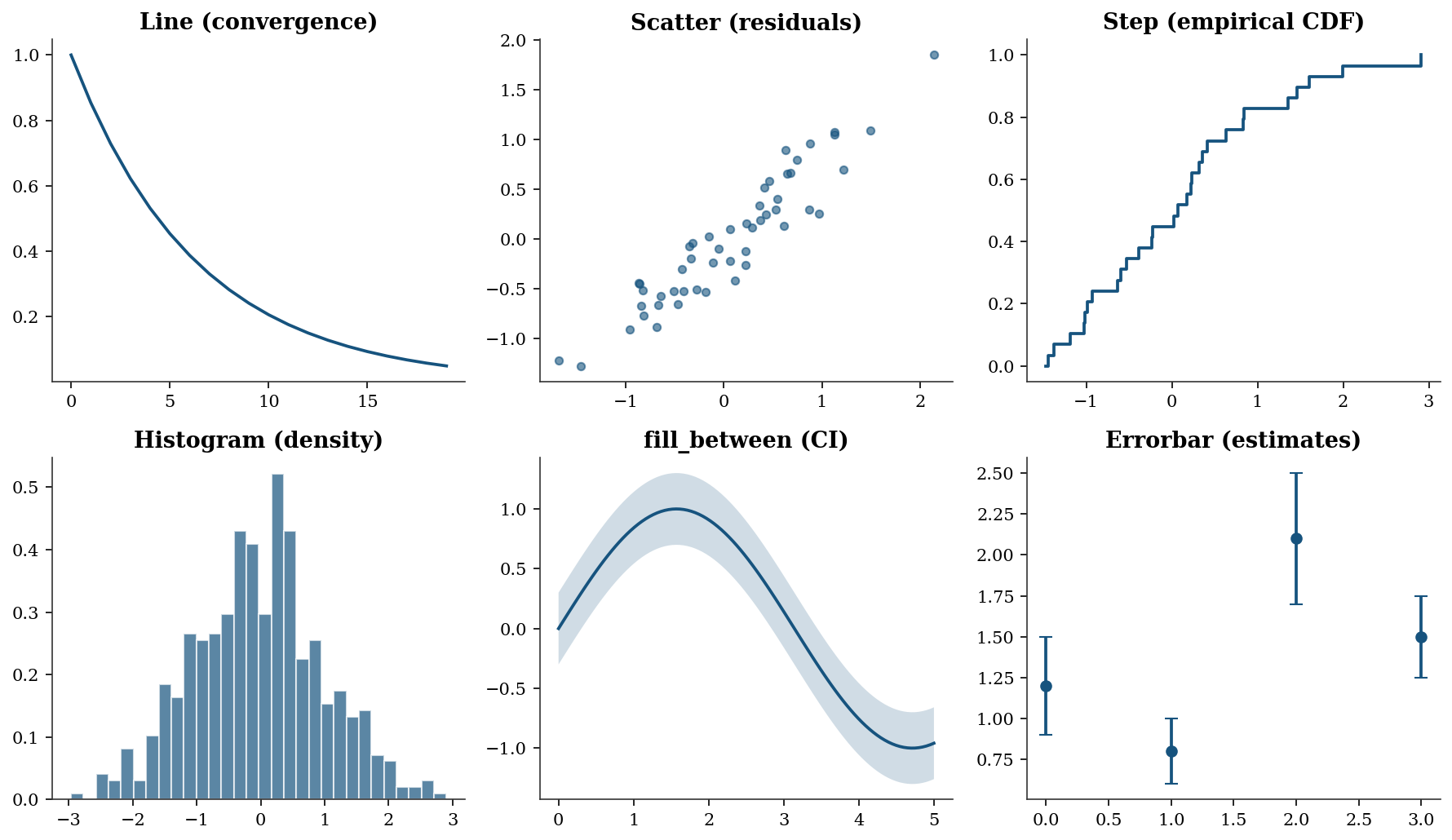

A.0.10 Common plot types used in the book

The chapters use a small set of plot types repeatedly. Here is a gallery with the calling conventions:

fig, axes = plt.subplots(2, 3, figsize=(12, 7))

# Line plot (convergence traces, Ch. 2-6)

axes[0, 0].plot(

np.arange(20),

np.exp(-np.linspace(0, 3, 20)),

)

axes[0, 0].set_title("Line (convergence)")

# Scatter plot (residuals, Ch. 11-12)

xs = rng.standard_normal(50)

ys = 0.8 * xs + 0.3 * rng.standard_normal(50)

axes[0, 1].scatter(xs, ys, alpha=0.6, s=20)

axes[0, 1].set_title("Scatter (residuals)")

# Step plot (CDFs, Ch. 9)

data = np.sort(rng.standard_normal(30))

axes[0, 2].step(

data,

np.linspace(0, 1, 30),

where="post",

)

axes[0, 2].set_title("Step (empirical CDF)")

# Histogram (distributions, Ch. 7-8)

axes[1, 0].hist(

rng.standard_normal(500),

bins=30, density=True, alpha=0.7,

edgecolor="white",

)

axes[1, 0].set_title("Histogram (density)")

# fill_between (confidence bands, Ch. 11)

xf = np.linspace(0, 5, 100)

yf = np.sin(xf)

axes[1, 1].plot(xf, yf)

axes[1, 1].fill_between(

xf, yf - 0.3, yf + 0.3, alpha=0.2,

)

axes[1, 1].set_title("fill_between (CI)")

# Errorbar (parameter estimates, Ch. 10)

means = [1.2, 0.8, 2.1, 1.5]

errs = [0.3, 0.2, 0.4, 0.25]

axes[1, 2].errorbar(

range(4), means, yerr=errs,

fmt="o", capsize=4,

)

axes[1, 2].set_title("Errorbar (estimates)")

fig.tight_layout()

plt.show()

When to use each plot type:

- Line plot — use for any quantity that evolves over an ordered index: optimization convergence traces (objective value vs iteration), power curves, or time series. The x-axis implies ordering.

- Scatter plot — use to reveal the relationship between two continuous variables: residuals vs fitted values, observed vs predicted, or bivariate distributions. No ordering is implied; the eye looks for correlation, clusters, or outliers.

- Step plot — use for quantities that jump at discrete points: empirical CDFs (Ch. 9), Kaplan–Meier survival curves (Ch. 18), or any piecewise-constant function.

where="post"means the step rises at the data point and stays flat until the next one. - Histogram — use to visualize the distribution of a single variable: MCMC posterior samples (Ch. 8), bootstrap replications (Ch. 9), or residual distributions (Ch. 11). Set

density=Trueto normalize the area to 1 so the histogram is comparable to a PDF overlay. - fill_between — use to show uncertainty bands around a curve: confidence intervals for regression lines (Ch. 11), credible intervals for posterior predictions (Ch. 8), or pointwise bootstrap bands (Ch. 9). The shaded region communicates “the true curve likely lies in here.”

- Errorbar — use to display point estimates with error bars: coefficient estimates \(\pm\) standard errors (Ch. 10), treatment effects with confidence intervals (Ch. 21–23), or any setting where you want to compare several estimates side-by-side with their uncertainty.

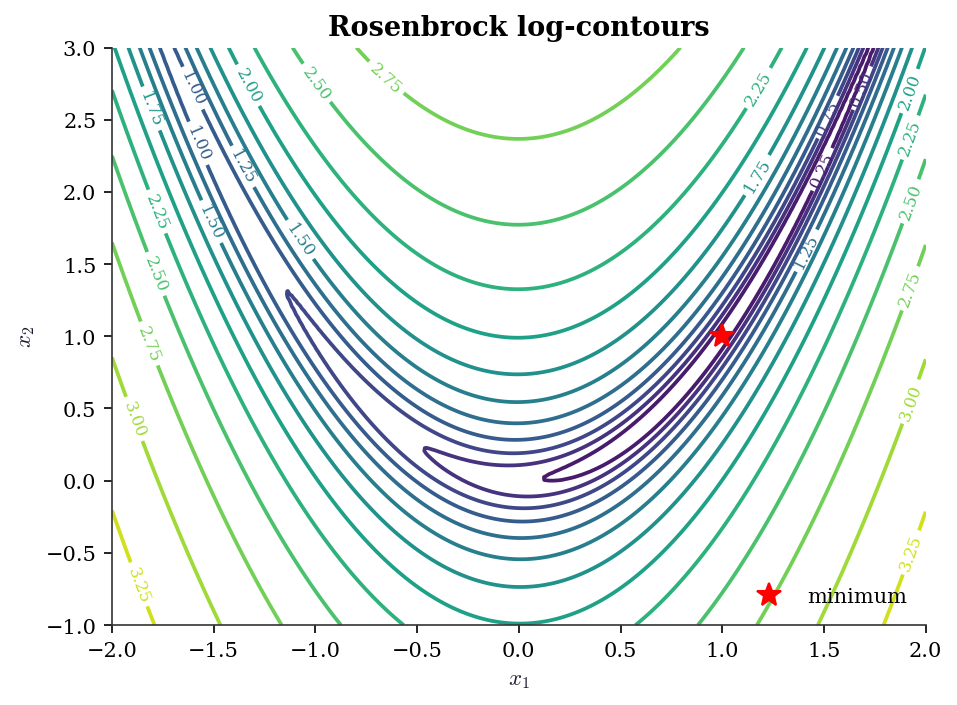

A.0.11 Contour plots

Contour plots visualize objective-function landscapes (Ch. 2–5):

x_grid = np.linspace(-2, 2, 200)

y_grid = np.linspace(-1, 3, 200)

Xg, Yg = np.meshgrid(x_grid, y_grid)

Z = (1 - Xg)**2 + 100 * (Yg - Xg**2)**2 # Rosenbrock

fig, ax = plt.subplots(figsize=(7, 5))

cs = ax.contour(

Xg, Yg, np.log10(Z + 1),

levels=15, cmap="viridis",

)

ax.clabel(cs, fontsize=8)

ax.plot(1, 1, "r*", markersize=12, label="minimum")

ax.set_xlabel("$x_1$")

ax.set_ylabel("$x_2$")

ax.set_title("Rosenbrock log-contours")

ax.legend()

plt.show()

A.0.12 Saving figures

fig.savefig("figure.pdf") # vector, for print

fig.savefig("figure.png") # raster, for screen

fig.savefig("figure.png", dpi=300, bbox_inches="tight")The book style sheet sets savefig.dpi: 300 and savefig.bbox: tight by default, so the explicit keyword arguments are rarely needed.

A.0.13 What book.mplstyle sets

The style file configures: serif fonts (Latin Modern Roman / Computer Modern), figure size 8 x 5 at 150 dpi, suppressed top and right spines, an 8-color cycle designed for grayscale readability with alternating solid/dashed/dot-dash/dotted line styles, outward-facing ticks, and frameless legends. Loading it via plt.style.use('assets/book.mplstyle') in each chapter’s import block ensures every figure in the book has a consistent appearance.

Floating Point and Conditioning

Every computation in this book runs on IEEE 754 double-precision floating point. Key facts:

- Machine epsilon: \(\epsilon_{\text{mach}} \approx 2.2 \times 10^{-16}\). Two numbers closer than this relative to their magnitude are indistinguishable.

- Representable range: doubles span roughly \(10^{-308}\) to \(10^{308}\). Operations outside this range produce underflow (silently flushed to zero) or overflow (

inf). - Catastrophic cancellation: \(a - b\) when \(a \approx b\) loses significant digits. This is why

np.logaddexp(0, x)is preferred overnp.log(1 + np.exp(x))for the log-sigmoid function.

print(f"Machine epsilon: {np.finfo(float).eps:.2e}")

print(f"Smallest positive: {np.finfo(float).tiny:.2e}")

print(f"Largest finite: {np.finfo(float).max:.2e}")Machine epsilon: 2.22e-16

Smallest positive: 2.23e-308

Largest finite: 1.80e+308A.0.14 Catastrophic cancellation in practice

# Naive vs stable log-sigmoid

x_vals = np.array([0.0, 20.0, 50.0, 100.0, 500.0, 710.0])

print(f"{'x':>6} {'naive':>22} {'stable':>22}")

for xv in x_vals:

naive = np.log(1 / (1 + np.exp(-xv)))

stable = -np.logaddexp(0, -xv)

print(f"{xv:6.0f} {naive:22.15e} {stable:22.15e}") x naive stable

0 -6.931471805599453e-01 -6.931471805599453e-01

20 -2.061153694291927e-09 -2.061153620314381e-09

50 0.000000000000000e+00 -1.928749847963918e-22

100 0.000000000000000e+00 -3.720075976020836e-44

500 0.000000000000000e+00 -7.124576406741286e-218

710 0.000000000000000e+00 -4.476286225675130e-309At \(x = 710\) the naive version overflows because np.exp(710) exceeds the double range. The stable version handles this correctly. This matters for log-likelihood evaluation in logistic regression (Ch. 12–13).

A.0.15 Condition number

The condition number \(\kappa(\mathbf{A}) = \|\mathbf{A}\| \cdot \|\mathbf{A}^{-1}\|\) measures how much a linear system \(\mathbf{Ax} = \mathbf{b}\) amplifies input errors. A system with \(\kappa = 10^k\) loses roughly \(k\) digits of accuracy.

# Well-conditioned vs ill-conditioned

print(f"Identity(5): kappa = "

f"{np.linalg.cond(np.eye(5)):.1f}")

print(f"Hilbert(5): kappa = "

f"{np.linalg.cond(linalg.hilbert(5)):.0f}")

print(f"Hilbert(10): kappa = "

f"{np.linalg.cond(linalg.hilbert(10)):.2e}")

print(f"Hilbert(15): kappa = "

f"{np.linalg.cond(linalg.hilbert(15)):.2e}")Identity(5): kappa = 1.0

Hilbert(5): kappa = 476607

Hilbert(10): kappa = 1.60e+13

Hilbert(15): kappa = 4.24e+17The Hilbert matrix is the classic example of near-singularity. By order 15 the condition number exceeds \(10^{17}\), meaning no digits in the solution are reliable. Condition numbers appear in: Ch. 2 (optimizer convergence speed depends on \(\kappa\) of the Hessian), Ch. 11 (multicollinearity diagnosis via VIF, which is a condition-number proxy), and Ch. 20 (weak instruments produce ill-conditioned moment matrices).

A.0.16 Useful safeguards

# log1p and expm1 avoid cancellation near zero

x_small = 1e-15

print(f"log(1 + x): {np.log(1 + x_small):.6e}")

print(f"log1p(x): {np.log1p(x_small):.6e}")

# logsumexp for stable log-sum-of-exponentials

from scipy.special import logsumexp

log_vals = np.array([1000, 1001, 1002])

print(f"\nlogsumexp: {logsumexp(log_vals):.6f}")

# naive would overflow:

# np.log(np.sum(np.exp(log_vals))) -> inflog(1 + x): 1.110223e-15

log1p(x): 1.000000e-15

logsumexp: 1002.407606Dense Linear Algebra (scipy.linalg)

SciPy’s linalg module wraps LAPACK and provides the decompositions used throughout the book. Prefer scipy.linalg over numpy.linalg — it is a strict superset with better LAPACK coverage and consistent error handling.

A.0.17 Key decompositions

| Decomposition | scipy call | Cost | Used in |

|---|---|---|---|

| LU | linalg.lu |

\(O(n^3)\) | General linear systems |

| Cholesky | linalg.cholesky |

\(O(n^3/3)\) | Positive-definite systems (Ch. 8, 14) |

| QR | linalg.qr |

\(O(mn^2)\) | OLS via QR (Ch. 11) |

| SVD | linalg.svd |

\(O(mn^2)\) | PCA (Ch. 19), pseudoinverse |

| Eigendecomposition | linalg.eigh |

\(O(n^3)\) | PCA, MANOVA (Ch. 19) |

A.0.18 Solving linear systems

A = np.array([[4.0, 2.0], [2.0, 3.0]])

b = np.array([1.0, 2.0])

# General solve (uses LU internally)

x = linalg.solve(A, b)

print(f"solve: x = {x.round(6)}")

# Positive-definite solve (uses Cholesky, ~2x faster)

x_pd = linalg.solve(

A, b, assume_a="pos",

)

print(f"solve PD: x = {x_pd.round(6)}")

# Verify

print(f"A @ x = {(A @ x).round(6)}, b = {b}")solve: x = [-0.125 0.75 ]

solve PD: x = [-0.125 0.75 ]

A @ x = [1. 2.], b = [1. 2.]assume_a="pos" tells linalg.solve the matrix is positive definite, so it uses Cholesky instead of LU — halving the flop count. This matters when solving covariance systems repeatedly (Ch. 8, Ch. 14).

A.0.19 Decomposition examples

A = np.array([[4.0, 2.0], [2.0, 3.0]])

# Cholesky

L = linalg.cholesky(A, lower=True)

print(f"Cholesky: L @ L.T = A? "

f"{np.allclose(L @ L.T, A)}")

# SVD

U, S, Vt = linalg.svd(A)

print(f"SVD singular values: {S.round(3)}")

print(f"Condition number: {S[0] / S[1]:.3f}")

# Eigendecomposition (symmetric)

eigvals, eigvecs = linalg.eigh(A)

print(f"Eigenvalues: {eigvals.round(3)}")Cholesky: L @ L.T = A? True

SVD singular values: [5.562 1.438]

Condition number: 3.866

Eigenvalues: [1.438 5.562]Use linalg.eigh (not linalg.eig) for symmetric matrices. It exploits symmetry for better speed and numerical stability, and guarantees real eigenvalues. The general linalg.eig returns complex values even for symmetric input due to rounding.

A.0.20 When to use scipy.linalg vs numpy.linalg

numpy.linalg covers basic operations (solve, eig, svd, norm, cond). scipy.linalg adds Cholesky with lower control, LU factorization, specialized solvers (solve_triangular, solve_banded, cho_solve), matrix functions (expm, logm), and the assume_a parameter for solve. Throughout this book, we import from scipy.linalg exclusively.

References: Trefethen and Bau (1997), Golub and Van Loan (2013).

scipy.optimize Quick Reference

The optimization chapters (Ch. 2–6) develop these methods in detail. This section is a lookup table.

A.0.21 minimize: unconstrained and constrained

| Method | Order | Gradient | Hessian | Best for | Chapter |

|---|---|---|---|---|---|

Nelder-Mead |

0 | No | No | Non-smooth, low-dim | 5 |

Powell |

0 | No | No | Non-smooth, moderate dim | 5 |

CG |

1 | Yes | No | Large-scale, smooth | 2 |

BFGS |

quasi-2 | Yes | No | General smooth, default | 2 |

L-BFGS-B |

quasi-2 | Yes | No | Large-scale with bounds | 4 |

Newton-CG |

2 | Yes | Yes/HVP | Moderate-scale, smooth | 2 |

trust-ncg |

2 | Yes | Yes | Small-to-moderate, smooth | 2 |

trust-krylov |

2 | Yes | HVP | Large-scale trust-region | 4 |

COBYLA |

0 | No | No | Constrained, no gradients | 3 |

SLSQP |

1 | Yes | No | Constrained, smooth | 3 |

trust-constr |

2 | Yes | Yes | Constrained, general | 3 |

The default when method is omitted is BFGS (if unconstrained without bounds), L-BFGS-B (if bounds are provided), or raises an error (if constraints are given). Always spell out method explicitly (STEERING.md §5.5).

# Basic minimize call

result = optimize.minimize(

fun=lambda x: (x[0] - 1)**2 + (x[1] - 2.5)**2,

x0=np.array([0.0, 0.0]),

method='BFGS',

)

print(f"x* = {result.x.round(6)}")

print(f"f(x*) = {result.fun:.2e}")

print(f"Converged: {result.success}")

print(f"Iterations: {result.nit}")x* = [1. 2.5]

f(x*) = 1.97e-15

Converged: True

Iterations: 2A.0.22 least_squares vs curve_fit

Both solve nonlinear least-squares problems (Ch. 6). least_squares is the general interface — you supply the residual vector \(\mathbf{r}(\mathbf{x})\) and optionally the Jacobian. curve_fit is a convenience wrapper for the common case of fitting a model function \(y = f(x; \boldsymbol{\theta})\) to data.

# least_squares: full control

def residuals(params, x, y):

a, b, c = params

return y - a * np.exp(-b * x) + c

x_data = np.linspace(0, 4, 50)

y_data = (2.5 * np.exp(-1.3 * x_data) + 0.5

+ 0.1 * rng.standard_normal(50))

res = optimize.least_squares(

fun=residuals,

x0=[1.0, 1.0, 0.0],

args=(x_data, y_data),

method='trf',

)

print(f"least_squares: params = {res.x.round(3)}")

print(f"Cost: {res.cost:.4f}")least_squares: params = [ 2.58 1.397 -0.519]

Cost: 0.2414| Feature | least_squares |

curve_fit |

|---|---|---|

| Input | Residual vector | Model function |

| Bounds | Yes | Yes |

| Jacobian | User-supplied or finite-diff | Auto (via least_squares) |

| Covariance of params | Manual from Jacobian | Returned as pcov |

| Robust losses | loss='huber', 'cauchy', etc. |

No |

A.0.23 root: nonlinear equations

optimize.root solves \(\mathbf{F}(\mathbf{x}) = \mathbf{0}\). For scalar equations use optimize.brentq (bracketing, guaranteed convergence) or optimize.newton (Newton–Raphson). These appear in Ch. 10 for solving score equations and in Ch. 18 for survival function inversion.

# Scalar root-finding: solve x - cos(x) = 0

root_val = optimize.brentq(

f=lambda x: x - np.cos(x),

a=0, b=1,

)

print(f"brentq: x = {root_val:.10f}")

print(f"verify: x - cos(x) = "

f"{root_val - np.cos(root_val):.2e}")brentq: x = 0.7390851332

verify: x - cos(x) = -7.88e-15A.0.24 The OptimizeResult object

All scipy.optimize functions return an OptimizeResult — a dictionary-like object with standardized fields:

| Attribute | Meaning |

|---|---|

.x |

Solution vector |

.fun |

Objective value at solution |

.success |

Whether the optimizer converged |

.message |

Human-readable convergence status |

.nit |

Number of iterations |

.nfev |

Number of function evaluations |

.jac |

Jacobian at solution (if computed) |

.hess_inv |

Inverse Hessian approximation (BFGS) |

Always check .success and .message before trusting .x. An optimizer that hits the iteration limit returns success=False — the solution may still be close to optimal, but you should not assume so without checking. This is a recurring theme in Ch. 2–6.

scipy.stats Quick Reference

A.0.25 The frozen distribution API

All distributions in scipy.stats follow the same pattern: create a frozen distribution object, then call methods on it. This is the single most important API pattern in the book.

# Create a frozen distribution

rv = stats.norm(loc=0, scale=1)

# Core methods (same for every distribution)

x = np.linspace(-3, 3, 7)

print("pdf:", rv.pdf(x).round(4))

print("cdf:", rv.cdf(x).round(4))

print("ppf (quantile):", rv.ppf([0.025, 0.5, 0.975]).round(4))

print("mean:", rv.mean(), " var:", rv.var())

print("interval(0.95):", rv.interval(0.95))

print("rvs:", rv.rvs(size=5, random_state=rng).round(3))pdf: [0.0044 0.054 0.242 0.3989 0.242 0.054 0.0044]

cdf: [0.0013 0.0228 0.1587 0.5 0.8413 0.9772 0.9987]

ppf (quantile): [-1.96 0. 1.96]

mean: 0.0 var: 1.0

interval(0.95): (np.float64(-1.959963984540054), np.float64(1.959963984540054))

rvs: [ 0.952 -2.252 -0.827 -0.782 -2.32 ]Discrete distributions use pmf (probability mass function) instead of pdf:

rv_pois = stats.poisson(mu=5)

print("pmf(3):", rv_pois.pmf(3).round(4))

print("cdf(3):", rv_pois.cdf(3).round(4))

print("mean:", rv_pois.mean(), " var:", rv_pois.var())pmf(3): 0.1404

cdf(3): 0.265

mean: 5.0 var: 5.0A.0.26 Distribution catalog

| Distribution | scipy call | Shape params | Used in |

|---|---|---|---|

| Normal | norm(loc, scale) |

— | Throughout |

| Student \(t\) | t(df) |

df |

Ch. 10–11 |

| Chi-squared | chi2(df) |

df |

Ch. 10 |

| \(F\) | f(dfn, dfd) |

dfn, dfd |

Ch. 10–11 |

| Gamma | gamma(a, scale=s) |

a |

Ch. 7, 18 |

| Beta | beta(a, b) |

a, b |

Ch. 7, 9 |

| Exponential | expon(scale=s) |

— | Ch. 18 |

| Weibull | weibull_min(c, scale=s) |

c |

Ch. 18 |

| Multivariate normal | multivariate_normal(mean, cov) |

— | Ch. 8, 19 |

| Poisson | poisson(mu) |

mu |

Ch. 12 |

| Binomial | binom(n, p) |

n, p |

Ch. 12 |

distributions = {

'Normal(0,1)': stats.norm(0, 1),

'Student t(5)': stats.t(df=5),

'Chi-sq(3)': stats.chi2(df=3),

'F(5,20)': stats.f(dfn=5, dfd=20),

'Gamma(2,1)': stats.gamma(a=2, scale=1),

'Exp(1)': stats.expon(scale=1),

}

print(f"{'Distribution':<15} {'Mean':>8} {'Var':>8}"

f" {'95% CI':>22}")

for name, rv in distributions.items():

ci = rv.interval(0.95)

print(f"{name:<15} {rv.mean():>8.3f} {rv.var():>8.3f}"

f" {'({:.2f}, {:.2f})'.format(*ci):>22}")Distribution Mean Var 95% CI

Normal(0,1) 0.000 1.000 (-1.96, 1.96)

Student t(5) 0.000 1.667 (-2.57, 2.57)

Chi-sq(3) 3.000 6.000 (0.22, 9.35)

F(5,20) 1.111 0.710 (0.16, 3.29)

Gamma(2,1) 2.000 2.000 (0.24, 5.57)

Exp(1) 1.000 1.000 (0.03, 3.69)A.0.27 Fitting distributions to data

# Generate data from a gamma distribution

data = stats.gamma.rvs(

a=2.5, scale=1.5,

size=500, random_state=rng,

)

# MLE fit

a_hat, loc_hat, scale_hat = stats.gamma.fit(

data, floc=0, # fix location to 0

)

print(f"True: a=2.500, scale=1.500")

print(f"MLE: a={a_hat:.3f}, scale={scale_hat:.3f}")True: a=2.500, scale=1.500

MLE: a=2.611, scale=1.395floc=0 fixes the location parameter — standard for distributions that are naturally non-negative. Without it, the optimizer may find a negative location that improves the likelihood but produces a nonsensical model.

A.0.28 Hypothesis tests catalog

| Test | scipy call | Null hypothesis |

|---|---|---|

| One-sample \(t\) | ttest_1samp(x, mu0) |

\(\mu = \mu_0\) |

| Two-sample \(t\) | ttest_ind(x, y) |

\(\mu_x = \mu_y\) |

| Welch \(t\) | ttest_ind(x, y, equal_var=False) |

\(\mu_x = \mu_y\) |

| Paired \(t\) | ttest_rel(x, y) |

\(\mu_{x-y} = 0\) |

| Chi-squared GOF | chisquare(obs, exp) |

Observed matches expected |

| \(F\)-test (ANOVA) | f_oneway(*groups) |

All group means equal |

| Pearson \(r\) | pearsonr(x, y) |

\(\rho = 0\) |

| Spearman \(\rho\) | spearmanr(x, y) |

Monotonic independence |

| KS test | kstest(x, cdf) |

\(x\) follows the given CDF |

| Shapiro–Wilk | shapiro(x) |

\(x\) is normally distributed |

| Mann–Whitney \(U\) | mannwhitneyu(x, y) |

Stochastic equality |

| Kruskal–Wallis | kruskal(*groups) |

Stochastic equality (\(k\) groups) |

A.0.29 Quasi-Monte Carlo

scipy.stats.qmc provides low-discrepancy sequences for numerical integration and space-filling experimental designs (Ch. 7):

from scipy.stats import qmc

sampler = qmc.Sobol(d=2, scramble=True, seed=rng)

points = sampler.random(64)

print(f"Sobol 64 points in [0,1]^2, "

f"discrepancy = {qmc.discrepancy(points):.6f}")Sobol 64 points in [0,1]^2, discrepancy = 0.000156Parametric Hypothesis Testing

A.0.30 The \(t\), \(F\), and \(\chi^2\) tests

These are the building blocks for Wald, score, and likelihood-ratio tests (Ch. 10).

# One-sample t-test

x = rng.normal(loc=0.5, scale=1, size=30)

t_stat, t_pval = stats.ttest_1samp(x, popmean=0)

print(f"t-test (H0: mu=0): t={t_stat:.3f}, "

f"p={t_pval:.4f}")

# Two-sample Welch t-test

y = rng.normal(loc=0, scale=1, size=30)

t2_stat, t2_pval = stats.ttest_ind(

x, y, equal_var=False,

)

print(f"Welch t-test: t={t2_stat:.3f}, "

f"p={t2_pval:.4f}")

# Chi-squared goodness of fit

observed = np.array([45, 35, 20])

expected = np.array([40, 40, 20])

chi2_stat, chi2_pval = stats.chisquare(

observed, f_exp=expected,

)

print(f"Chi-sq test: stat={chi2_stat:.3f}, "

f"p={chi2_pval:.4f}")t-test (H0: mu=0): t=1.393, p=0.1742

Welch t-test: t=1.448, p=0.1531

Chi-sq test: stat=1.250, p=0.5353A.0.31 One-way ANOVA (\(F\)-test)

The one-way ANOVA tests whether \(k\) groups have the same mean. Under the null, the \(F\) statistic follows an \(F_{k-1, N-k}\) distribution. This is the multivariate generalization of the two-sample \(t\)-test and appears as a building block in Ch. 10–11.

group_a = rng.normal(loc=5.0, scale=1.0, size=30)

group_b = rng.normal(loc=5.5, scale=1.0, size=30)

group_c = rng.normal(loc=6.0, scale=1.0, size=30)

f_stat, f_pval = stats.f_oneway(

group_a, group_b, group_c,

)

print(f"One-way ANOVA: F={f_stat:.3f}, "

f"p={f_pval:.4f}")One-way ANOVA: F=6.535, p=0.0023Nonparametric Tests

# Mann-Whitney U (two-sample rank test)

u_stat, u_pval = stats.mannwhitneyu(

x, y, alternative='two-sided',

)

print(f"Mann-Whitney U: stat={u_stat:.1f}, "

f"p={u_pval:.4f}")

# Kolmogorov-Smirnov (distribution comparison)

ks_stat, ks_pval = stats.kstest(

x, 'norm', args=(x.mean(), x.std()),

)

print(f"KS test: stat={ks_stat:.3f}, "

f"p={ks_pval:.4f}")

# Shapiro-Wilk (normality)

sw_stat, sw_pval = stats.shapiro(x)

print(f"Shapiro-Wilk: stat={sw_stat:.3f}, "

f"p={sw_pval:.4f}")

# Kruskal-Wallis (k-sample rank test)

kw_stat, kw_pval = stats.kruskal(

group_a, group_b, group_c,

)

print(f"Kruskal-Wallis: stat={kw_stat:.3f}, "

f"p={kw_pval:.4f}")Mann-Whitney U: stat=561.0, p=0.1023

KS test: stat=0.124, p=0.7009

Shapiro-Wilk: stat=0.981, p=0.8527

Kruskal-Wallis: stat=11.872, p=0.0026Correlation and Dependence

x_corr = rng.standard_normal(100)

y_corr = 0.7 * x_corr + 0.3 * rng.standard_normal(100)

# Pearson (linear association)

r, p = stats.pearsonr(x_corr, y_corr)

print(f"Pearson: r={r:.3f}, p={p:.4f}")

# Spearman (monotonic association, rank-based)

rho, p_s = stats.spearmanr(x_corr, y_corr)

print(f"Spearman: rho={rho:.3f}, p={p_s:.4f}")

# Kendall (concordance, rank-based)

tau, p_k = stats.kendalltau(x_corr, y_corr)

print(f"Kendall: tau={tau:.3f}, p={p_k:.4f}")Pearson: r=0.933, p=0.0000

Spearman: rho=0.928, p=0.0000

Kendall: tau=0.774, p=0.0000A.0.32 Partial correlation

Partial correlation measures the linear association between two variables after removing the effect of one or more confounders. It is used in Ch. 11 (regression diagnostics) and Ch. 17 (testing for Granger-causal relationships after conditioning on other series).

# Partial correlation of x and y given z

z_corr = 0.5 * x_corr + 0.5 * rng.standard_normal(100)

# Residualize x and y on z

def residualize(var, controls):

"""Residuals from OLS of var on controls."""

X_ctrl = np.column_stack(controls)

X_aug = np.column_stack([np.ones(len(var)), X_ctrl])

beta = np.linalg.lstsq(X_aug, var, rcond=None)[0]

return var - X_aug @ beta

x_resid = residualize(x_corr, [z_corr])

y_resid = residualize(y_corr, [z_corr])

r_partial, p_partial = stats.pearsonr(x_resid, y_resid)

print(f"Partial corr (x,y | z): "

f"r={r_partial:.3f}, p={p_partial:.4f}")

print(f"Raw Pearson (x,y): "

f"r={r:.3f}")Partial corr (x,y | z): r=0.851, p=0.0000

Raw Pearson (x,y): r=0.933The partial correlation is typically lower than the raw correlation because the confounder \(z\) explains some of the apparent association.

A.0.33 Correlation matrix

data_corr = np.column_stack([x_corr, y_corr, z_corr])

R = np.corrcoef(data_corr, rowvar=False)

print("Correlation matrix:")

print(R.round(3))Correlation matrix:

[[1. 0.933 0.766]

[0.933 1. 0.729]

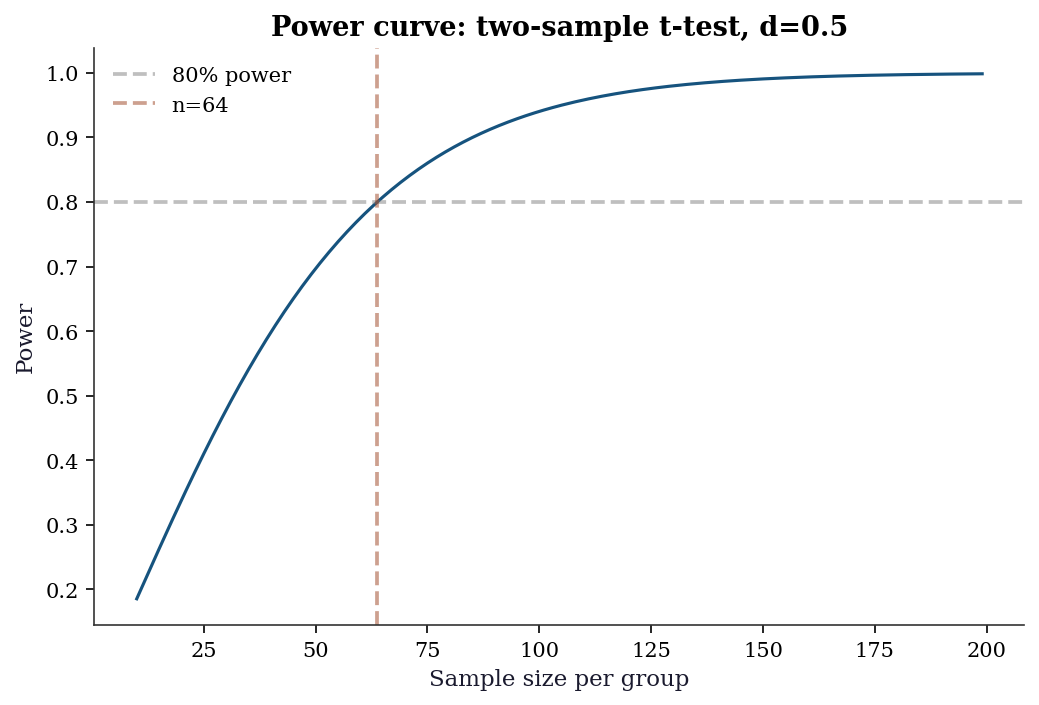

[0.766 0.729 1. ]]Power and Sample Size

Statistical power = probability of detecting a true effect. For a two-sample \(t\)-test with effect size \(d = (\mu_1 - \mu_2)/\sigma\):

from statsmodels.stats.power import TTestIndPower

power_analysis = TTestIndPower()

# Sample size for 80% power, effect size d=0.5, alpha=0.05

n_needed = power_analysis.solve_power(

effect_size=0.5, alpha=0.05, power=0.8,

alternative='two-sided',

)

print(f"Sample size needed (per group): {n_needed:.0f}")

# Power for n=50 per group

power = power_analysis.solve_power(

effect_size=0.5, alpha=0.05, nobs1=50,

alternative='two-sided',

)

print(f"Power with n=50: {power:.3f}")Sample size needed (per group): 64

Power with n=50: 0.697fig, ax = plt.subplots()

ns = np.arange(10, 200)

powers = [

power_analysis.solve_power(

0.5, alpha=0.05, nobs1=n_,

alternative='two-sided',

)

for n_ in ns

]

ax.plot(ns, powers, linewidth=1.5)

ax.axhline(

0.8, color="gray", linestyle="--",

alpha=0.5, label="80% power",

)

ax.axvline(

n_needed, color="C1", linestyle="--",

alpha=0.5, label=f"n={n_needed:.0f}",

)

ax.set_xlabel("Sample size per group")

ax.set_ylabel("Power")

ax.set_title("Power curve: two-sample t-test, d=0.5")

ax.legend()

plt.show()

Random Number Generation

The book uses the modern numpy.random.Generator API exclusively (STEERING.md §5.2). The legacy np.random.seed() / np.random.randn() API is never used.

# The canonical pattern

rng = np.random.default_rng(42)

# Key methods

print(f"Normal: {rng.standard_normal(3).round(3)}")

print(f"Uniform: {rng.uniform(0, 1, 3).round(3)}")

print(f"Poisson: {rng.poisson(5, 3)}")

print(f"Binomial: {rng.binomial(10, 0.3, 3)}")

print(f"Choice: "

f"{rng.choice([1, 2, 3, 4], 3, replace=True)}")

print(f"Permute: "

f"{rng.permutation([10, 20, 30, 40, 50])}")

# Reproducibility

rng1 = np.random.default_rng(42)

rng2 = np.random.default_rng(42)

print(f"\nReproducible: "

f"{np.array_equal(rng1.standard_normal(5), rng2.standard_normal(5))}")Normal: [ 0.305 -1.04 0.75 ]

Uniform: [0.697 0.094 0.976]

Poisson: [7 3 9]

Binomial: [2 4 4]

Choice: [2 4 2]

Permute: [10 40 50 30 20]

Reproducible: TrueKey difference from legacy API: Generator uses the PCG64 PRNG (better statistical properties than Mersenne Twister). Each Generator instance maintains its own state, so multiple generators can run independently without global state conflicts.

A.0.34 Passing rng to library functions

scipy and statsmodels functions that accept randomness use the random_state parameter:

# scipy.stats distributions

samples = stats.norm.rvs(

loc=0, scale=1, size=5,

random_state=rng,

)

print(f"scipy.stats.rvs: {samples.round(3)}")

# scipy.stats.bootstrap (Ch. 9)

data_boot = (rng.standard_normal(50),)

res = stats.bootstrap(

data_boot, np.mean,

n_resamples=999,

random_state=rng,

method='percentile',

)

print(f"Bootstrap CI: ({res.confidence_interval.low:.3f},"

f" {res.confidence_interval.high:.3f})")scipy.stats.rvs: [ 1.129 -0.114 -0.84 -0.824 0.651]

Bootstrap CI: (-0.201, 0.169)Statsmodels Patterns

Statsmodels is the primary library for chapters 10–18. Its API follows a distinctive pattern that differs from scipy’s functional style.

A.0.35 The .fit() → results pattern

Every statsmodels model follows the same two-step workflow: construct the model, then call .fit() to obtain a results object. All inference — coefficients, standard errors, confidence intervals, hypothesis tests — lives on the results object.

# Generate data

n = 100

x1 = rng.standard_normal(n)

x2 = rng.standard_normal(n)

y = 1.5 + 2.0 * x1 - 0.5 * x2 + rng.standard_normal(n)

# Array API: add constant manually

X = sm.add_constant(np.column_stack([x1, x2]))

model = sm.OLS(endog=y, exog=X)

results = model.fit()

print(results.summary().tables[1])==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 1.6404 0.099 16.498 0.000 1.443 1.838

x1 1.9633 0.102 19.326 0.000 1.762 2.165

x2 -0.4584 0.094 -4.853 0.000 -0.646 -0.271

==============================================================================A.0.36 from_formula vs array API

Statsmodels supports both an array API (shown above) and a formula API using patsy/formulaic:

import pandas as pd

df = pd.DataFrame({'y': y, 'x1': x1, 'x2': x2})

# Formula API: intercept is automatic

results_f = sm.OLS.from_formula(

'y ~ x1 + x2', data=df,

).fit()

print(f"Array API params: "

f"{results.params.round(3)}")

print(f"Formula API params: "

f"{results_f.params.round(3)}")Array API params: [ 1.64 1.963 -0.458]

Formula API params: Intercept 1.640

x1 1.963

x2 -0.458

dtype: float64The formula API adds the intercept automatically (~ 1 + is implied). Use y ~ x1 + x2 - 1 to suppress it. The array API requires sm.add_constant() explicitly.

In this book, the array API is preferred for transparency — the reader sees exactly what the design matrix \(\mathbf{X}\) contains. The formula API appears in examples where it makes the model specification more readable, particularly for interaction terms and categorical variables.

A.0.37 The results object

The results object carries everything downstream analysis needs:

print(f"Coefficients: {results.params.round(3)}")

print(f"Std errors: {results.bse.round(3)}")

print(f"t-statistics: {results.tvalues.round(3)}")

print(f"p-values: {results.pvalues.round(4)}")

print(f"R-squared: {results.rsquared:.4f}")

print(f"AIC: {results.aic:.1f}")

print(f"BIC: {results.bic:.1f}")

print(f"Log-likelihood:{results.llf:.1f}")

print(f"Residuals: {results.resid[:5].round(3)}")Coefficients: [ 1.64 1.963 -0.458]

Std errors: [0.099 0.102 0.094]

t-statistics: [16.498 19.326 -4.853]

p-values: [0. 0. 0.]

R-squared: 0.8053

AIC: 285.0

BIC: 292.8

Log-likelihood:-139.5

Residuals: [0.098 0.103 0.146 0.091 2.21 ]A.0.38 Complete worked example: fit, read, extract

The following example walks through the full OLS workflow — fitting a model, reading the summary table column by column, and extracting specific quantities programmatically for downstream use.

# Generate data with known coefficients

n_ex = 200

rng_ex = np.random.default_rng(99)

x1_ex = rng_ex.standard_normal(n_ex)

x2_ex = rng_ex.uniform(0, 10, n_ex)

# True model: y = 5 + 2*x1 - 0.3*x2 + noise

y_ex = (5.0 + 2.0 * x1_ex - 0.3 * x2_ex

+ rng_ex.standard_normal(n_ex))

# Build design matrix and fit

X_ex = sm.add_constant(

np.column_stack([x1_ex, x2_ex])

)

res_ex = sm.OLS(endog=y_ex, exog=X_ex).fit()

# --- Reading the summary table ---

print(res_ex.summary().tables[1])

print()

# Column-by-column explanation:

# coef = point estimate (beta-hat)

# std err = standard error of the estimate

# t = coef / std err (Wald statistic)

# P>|t| = two-sided p-value for H0: coef = 0

# [0.025 = lower bound of 95% confidence interval

# 0.975] = upper bound of 95% confidence interval

# --- Extracting specific values ---

# Coefficient for x1 (index 1, since index 0 is intercept)

beta1_hat = res_ex.params[1]

se1 = res_ex.bse[1]

pval1 = res_ex.pvalues[1]

print(f"x1 coefficient: {beta1_hat:.4f}")

print(f"x1 std error: {se1:.4f}")

print(f"x1 p-value: {pval1:.6f}")

# Confidence interval for x2 (index 2)

ci = res_ex.conf_int(alpha=0.05)

print(f"x2 95% CI: [{ci[2, 0]:.4f}, "

f"{ci[2, 1]:.4f}]")

# Model-level: R-squared and F-test

print(f"R-squared: {res_ex.rsquared:.4f}")

print(f"F-statistic: {res_ex.fvalue:.2f}")

print(f"F p-value: {res_ex.f_pvalue:.2e}")==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 4.9491 0.142 34.975 0.000 4.670 5.228

x1 1.9799 0.071 27.986 0.000 1.840 2.119

x2 -0.2727 0.024 -11.584 0.000 -0.319 -0.226

==============================================================================

x1 coefficient: 1.9799

x1 std error: 0.0707

x1 p-value: 0.000000

x2 95% CI: [-0.3192, -0.2263]

R-squared: 0.8152

F-statistic: 434.48

F p-value: 5.92e-73The key pattern: results.params[j] gives the \(j\)-th coefficient, results.bse[j] its standard error, results.pvalues[j] its \(p\)-value, and results.conf_int()[j] its confidence interval. Index 0 is always the intercept (if add_constant was used). These programmatic accessors are essential when you need to feed regression output into further computation — plotting coefficient comparisons, computing marginal effects manually, or building test statistics from multiple models.

A.0.39 Covariance type options

The default cov_type='nonrobust' assumes homoscedastic, independent errors. This is almost never defensible with real data. Statsmodels provides several robust alternatives:

cov_type |

Assumes | Use when |

|---|---|---|

'nonrobust' |

Homoscedastic, independent | Textbook exercises only |

'HC0' |

Heteroscedastic | White’s original estimator |

'HC1' |

Heteroscedastic | Small-sample correction (\(n/(n-k)\)) |

'HC3' |

Heteroscedastic | Preferred for small samples (Ch. 11) |

'HAC' |

Heteroscedastic + autocorrelated | Time series (Ch. 15–17) |

'cluster' |

Clustered errors | Grouped data (Ch. 14) |

# Compare standard errors under different assumptions

for cov in ['nonrobust', 'HC0', 'HC3']:

res = model.fit(cov_type=cov)

print(f"{cov:>12}: SE = {res.bse.round(4)}") nonrobust: SE = [0.0994 0.1016 0.0944]

HC0: SE = [0.0981 0.0944 0.0915]

HC3: SE = [0.1011 0.0989 0.0963]Always specify cov_type explicitly. Relying on the default is a common source of overconfident inference. See Ch. 11 for a detailed treatment.

A.0.40 Hypothesis testing on the results object

# Wald test: beta_1 = 2 (the true value)

t_test = results.t_test('x1 = 2')

print(f"t-test (beta_1=2): "

f"t={float(t_test.tvalue):.3f}, "

f"p={float(t_test.pvalue):.4f}")

# F-test: joint test that x1 = 0 and x2 = 0

f_test = results.f_test('x1 = 0, x2 = 0')

print(f"F-test (all slopes=0): "

f"F={float(f_test.fvalue):.3f}, "

f"p={float(f_test.pvalue):.6f}")

# Confidence intervals

print(f"\n95% confidence intervals:\n"

f"{results.conf_int(alpha=0.05).round(3)}")t-test (beta_1=2): t=-0.361, p=0.7185

F-test (all slopes=0): F=200.567, p=0.000000

95% confidence intervals:

[[ 1.443 1.838]

[ 1.762 2.165]

[-0.646 -0.271]]A.0.41 Marginal effects

For nonlinear models (Ch. 12–13), coefficients are not directly interpretable as marginal effects. The get_margeff() method computes average marginal effects:

# Logistic regression example

y_binary = (y > y.mean()).astype(int)

logit_model = sm.Logit(endog=y_binary, exog=X)

logit_results = logit_model.fit(disp=0)

mfx = logit_results.get_margeff(at='overall')

print(mfx.summary()) Logit Marginal Effects

=====================================

Dep. Variable: y

Method: dydx

At: overall

==============================================================================

dy/dx std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

x1 0.3560 0.033 10.729 0.000 0.291 0.421

x2 -0.0773 0.031 -2.471 0.013 -0.139 -0.016

==============================================================================The at='overall' option computes average marginal effects (AME) — the mean of the marginal effect evaluated at each observation. This is the most common choice. at='mean' evaluates at the sample mean of all covariates, which is simpler but potentially misleading for non-representative “average” individuals.

A.0.42 Reading summary() output

The summary() method produces three tables. The top table reports model-level statistics (R-squared, F-statistic, AIC, BIC, log-likelihood, Durbin–Watson). The middle table reports per-coefficient results (estimate, standard error, \(t\)-statistic, \(p\)-value, and 95% confidence interval). The bottom table reports omnibus diagnostics (Omnibus test, Jarque–Bera, skewness, kurtosis, condition number).

Key quantities to check immediately:

- R-squared vs Adjusted R-squared: a large gap signals overfitting. Adjusted R-squared penalizes for the number of predictors.

- F-statistic \(p\)-value: tests whether the model as a whole explains more variance than an intercept-only model. A non-significant \(F\)-test means none of the predictors matter jointly.

- Condition number: large values (\(>30\)) indicate multicollinearity. See Ch. 11 for VIF-based diagnosis.

- Durbin–Watson: values near 2 indicate no autocorrelation in residuals. Values near 0 or 4 indicate positive or negative autocorrelation respectively — a warning sign for cross-sectional models and a modeling choice for time-series models (Ch. 15).

A.0.43 Predictions and diagnostics

# Point predictions with confidence intervals

predictions = results.get_prediction(X[:5])

pred_summary = predictions.summary_frame(alpha=0.05)

print(pred_summary[

['mean', 'mean_ci_lower', 'mean_ci_upper']

].round(3)) mean mean_ci_lower mean_ci_upper

0 3.409 3.012 3.807

1 -0.534 -0.826 -0.243

2 -0.739 -1.107 -0.371

3 1.577 1.282 1.871

4 3.134 2.822 3.446A.0.44 The statsmodels diagnostic toolkit

Statsmodels provides diagnostic tests as standalone functions and as methods on results objects:

from statsmodels.stats.diagnostic import (

het_breuschpagan,

acorr_breusch_godfrey,

)

from statsmodels.stats.stattools import (

durbin_watson,

)

# Breusch-Pagan test for heteroscedasticity

bp_stat, bp_pval, _, _ = het_breuschpagan(

results.resid, results.model.exog,

)

print(f"Breusch-Pagan: stat={bp_stat:.3f}, "

f"p={bp_pval:.4f}")

# Durbin-Watson test for autocorrelation

dw = durbin_watson(results.resid)

print(f"Durbin-Watson: {dw:.3f} "

f"(~2 = no autocorrelation)")Breusch-Pagan: stat=1.011, p=0.6032

Durbin-Watson: 2.200 (~2 = no autocorrelation)These diagnostics are developed fully in Ch. 11 (regression diagnostics) and Ch. 15 (time-series residual diagnostics).

Environment and Reproducibility Checklist

Every code block in this book was executed in the environment defined by requirements.txt. To reproduce results:

uv venv .venv

source .venv/bin/activate

uv pip install -r requirements.txtThe key packages and their roles:

| Package | Role | Primary chapters |

|---|---|---|

numpy |

Array computation | All |

scipy |

Optimization, statistics, linear algebra | All |

statsmodels |

Statistical models, inference | 10–18 |

linearmodels |

IV, panel data | 20–22 |

matplotlib |

Plotting | All |

pandas |

Data frames | 10–23 |

scikit-learn |

Pipeline, datasets | 1, datasets elsewhere |

Verify your environment matches:

import scipy

import statsmodels

print(f"NumPy: {np.__version__}")

print(f"SciPy: {scipy.__version__}")

print(f"statsmodels: {statsmodels.__version__}")NumPy: 2.2.6

SciPy: 1.14.1

statsmodels: 0.14.4